With the release of WorldACD’s air cargo performance results for May, the slowdown from last year’s consistent double-digit increases is undeniable. Although volumes are still increasing year-over-year, the increases are significantly less than those seen during 2017.

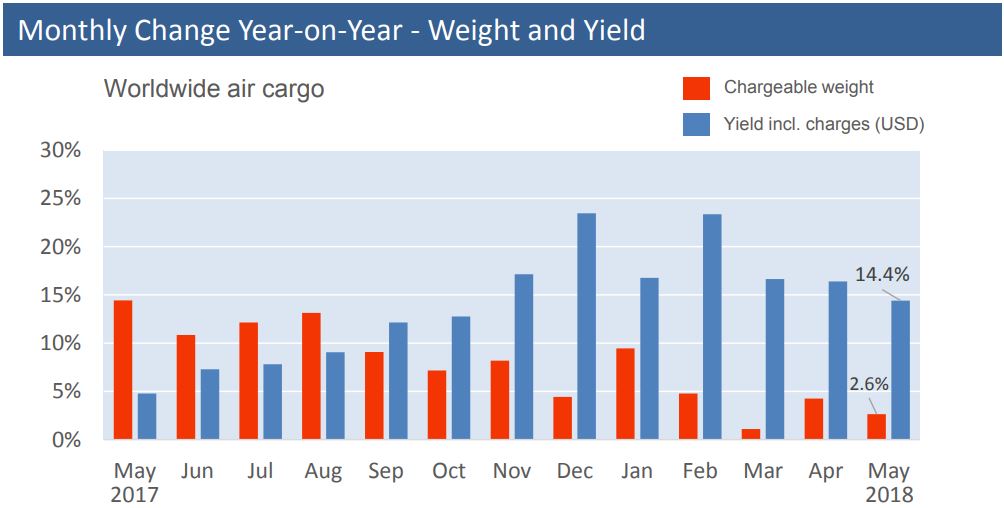

Air cargo volumes worldwide increased by 2.6 percent y-o-y in May, down from the nearly 15 percent y-o-y increase reported for May 2017, as year-over-year comparisons have become more difficult in 2018 thanks to the especially strong 2017 growth.  Worldwide, air cargo yields were up 14% year-over-year in US dollars for May but were 3% lower compared to April 2018. While yield growth seems healthy, it’s important to note that yield growth is currency dependent, and in euros, yields were up by a smaller 7 percent.

Worldwide, air cargo yields were up 14% year-over-year in US dollars for May but were 3% lower compared to April 2018. While yield growth seems healthy, it’s important to note that yield growth is currency dependent, and in euros, yields were up by a smaller 7 percent.

Turning to the airfreight price index from Drewry, average freight rates for East-West routes weakened month-to-month by US$0.03 but were still up by 10.7 percent y-o-y to $2.70. This is one area that is likely to continue its robust growth through at least June, and Drewry reports that it expects rates “to rise in June on the back of higher trans-Pacific rates.”

Is the party really over?

In its overview of May air cargo performance, WorldACD asked the question that has been rehashed repeatedly as traffic growth has slowed and protectionist rhetoric has increased in 2018: “Is the party really over?” With these most recent results, the slowdown from last year’s consistent double-digit increases is undeniable – while volumes are still increasing year-over-year, the increases are significantly less than those seen during 2017.

Preliminary results reported by some carriers, airports, and handlers suggested that cargo growth has remained fairly strong through May, but WorldACD’s May report paints a much more mixed picture. Air cargo volumes worldwide increased by a narrow 2.6% y-o-y in May. However, when considering volumes jumped nearly 15% y-o-y in May 2017, it becomes clear that May 2018 volumes are still substantially greater than two-years prior.

Turning now to yields, Worldwide, air cargo yields were up 14% year-over-year in US dollars for May but were 3% lower compared to April 2018. While yield growth seems healthy, it’s important to note that yield growth is currency dependent, and in euros, yields were up by a smaller 7%.

Of course, some regions performed better than others during May. Certain origin countries including the US, Japan, Canada, Brazil, and Chile all saw outgoing air cargo volumes at or near double-digit levels, with Chile reporting a particularly large increase of 29.0% y-o-y. Meanwhile, China and Russia both saw y-o-y declines in outgoing volumes. However, at least in the Americas, the volume increases were offset by smaller yield improvements “well below 10%, much lower than elsewhere in the world,” WorldACD noted.

Another interesting note from WorldACD’s May analysis comes from the comparison between GDP growth and air cargo volumes. Despite conventional wisdom tying air cargo volumes to economic performance metrics like GDP growth, some of the countries recording the strongest increases in cargo volumes have seen only modest GDP growth – for example, Brazil’s first quarter GDP growth was only 1.2%, despite 13.7% and 13.9% increases in outgoing and incoming air cargo volume growth, respectively. Meanwhile, China had particularly strong GDP growth of 6.8%, but outgoing volumes declined by 0.8%, indicating that “it is no longer possible to use a general ration between GDP-growth and air cargo growth.”

Turning to the air freight price index from Drewry, average freight rates for East-West routes weakened month-to-month by US$0.03 but were still up by 10.7% y-o-y to $2.70. This is one area that is likely to continue its robust growth through at least June, and Drewry reports that it expects rates “to rise in June on the back of higher trans-Pacific rates.”

Certainly, several factors still weigh in favor of increasing rates through June. As we reported late last month, the grounding of Nippon Cargo Airlines’ (NCA’s) fleet of eleven 747Fs has pushed air freight rates ex-Shanghai up significantly, and it remains unclear when the carrier will resume operations.

Another source of uncertainty the air cargo market faces relates to the now pervasive protectionist sentiment and impending tariffs, which could put a damper on demand. US Customs and Border Protection is set to begin collecting additional duties on certain Chinese imports on 6 July, so the full impact from tariffs is unlikely to become clear until August, when the first results from July are released.

.